Time to YOLO again?

Bitcoin signal or late bloomer?, BTFP loans as a booster, Ripple and the SEC, DalliPay and memes.

Let’s gooo 🎢 What to expect:

Knowledge-Level : 🟢 Beginner| 🟡 Advanced | 🔵 Expert

Insight DeFi on Social Media: LinkedIn / Instagram / Twitter / YouTube / Telegram

🟢 Market Update: Is Bitcoin sending a signal or just lagging?

written by Pascal Hügli

Currently, the macro world is a constant up and down. Just a week ago Friday, the yield on the 10-year Treasury bond rose from 3.94% to 4.06%. And the yield on the 2-year U.S. Treasury paper also climbed to over 5%. This matched levels seen in early March during the Silicon Valley Bank collapse - an interest rate so high, we haven’t seen it since 2007.

Then this week, the latest consumer price data was released and it came in with a bang. While CPI slowed from 4% to 3% (3.1% was expected) and the core inflation index also fell from 5.3% to 4.8%, all seemed right with the world again from the perspective of risk assets investors.

After all, the inflation figures, which have now fallen consistently for 12 months, suggest that the U.S. Federal Reserve appears to be successful in its aggressive fight against inflation. Nevertheless, the market expects another rate hike by the Fed in July with a very high probability (94%).

It is worth mentioning that Bitcoin has not really reacted to this inflation data, which should have actually been positive for crypto assets. In theory, easing inflation should benefit crypto assets more than stocks, as the impact is leaning positively towards more liquidity, while being negative for earnings growth. But why has BTC barely moved higher? Is bitcoin simply still lagging behind or should this fact rather be interpreted as a signal that immediate market disruptions are on the imminent horizon?

Similarly impressive is the way the Swiss franc is appreciating against the US dollar just in the last few days. This fact is also seen by some as an indication that something could be up. After all, the Swiss franc is still considered the "safest haven" within the fiat world. Compared to global bonds, the CHF has started to rally, which could be an indication that forward-looking investors have started to abandon the ship of long-dated fiat government bonds:

What is striking is that equities are doing well at the moment. In recent weeks they have lost their correlation to the total of global central bank balance sheets. As the chart below shows, a correlation has been unmistakable around since the financial crisis. So are equities overvalued right now, and will the drying up of liquidity from declining global central bank balance sheets soon catch up with them?

The next few weeks will show. It should not be forgotten, and we have been beating this drum for a while, that while central bank balance sheets are an important component of global financial liquidity, they do not paint the whole picture by a long shot. There are many other aspects to consider and we take a closer look at some of them again in this month's Liquidity Corner.

Bullish or bearish, then? If you zoom out, you will quickly come across some bullish factors:

The aggressive interest rate policy of the U.S. Federal Reserve is more reaching the end than being at the beginning.

A spot BTC ETF is being considered in the U.S., which could bring new capital into the crypto world.

The world's largest asset managers are bullish on BTC, which in turn is massively boosting its reputation in the traditional financial world.

Many investors are still in a bear market shock, which is why they are still sitting on the sidelines with their capital.

Forced liquidations (FTX, Celsius, Luna, 3AC, etc.) have largely been completed and a capitulation has taken place in this respect.

Retail investors are not yet back in the market (see e.g. Google Trends).

Bitcoin halving is only about 300 days away.

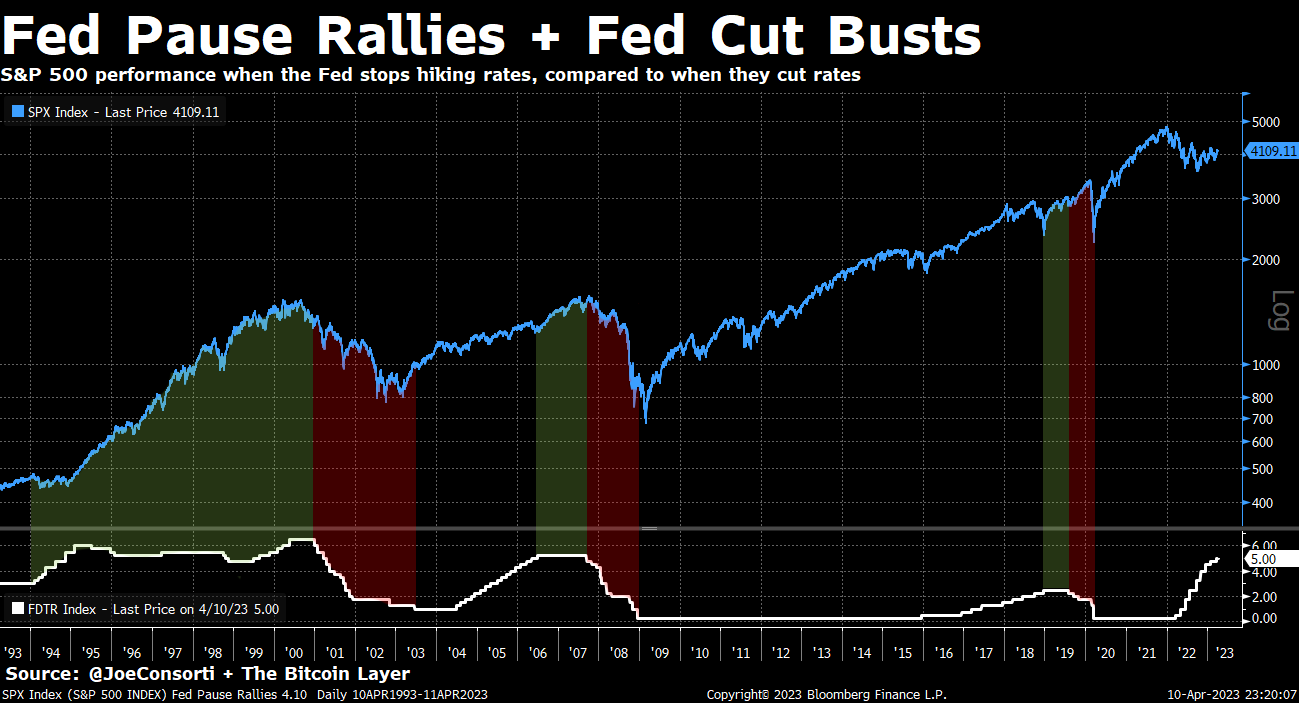

Despite all the possible euphoria, however, it should be noted: Market rallies take place when the U.S. Federal Reserve takes a pause regarding the hiking of its interest rates (which, arguably, has just happened, although they could be hiked in July yet again). Historically, when central banks cut rates, markets have corrected first:

So it does indeed seem to be the case that the current relief rally during interest rate breaks make the lag effects forgettable in the short term. After all, it takes 12 to 18 months for them to make themselves felt in the economy. Let's remember that this time around last year, the federal funds rate was still only at 1.58%.

🟢 Liquidity Corner: BFTP loans continue to boost markets

written by Pascal Hügli

A look at the numbers:

Net financial liquidity in the U.S. (with the BTFP emergency lending program):

June 29 (past newsletter issue): $5,899 billion

July 13 (current newsletter issue): $5,988 billion

️↗️Increase of $89 billion.

Broken down even further here:

Total balance sheet* of the Federal Reserve:

June 28 (past newsletter issue): $8,340 billion

July 12 (current newsletter issue): $8,296 billion

↙️Reduction $44 billion

U.S. reverse repo programs:

June 29 (past newsletter issue): $1,935 billion

July 13 (current newsletter issue): $1,767 billion

↙️Reduction of $168 billion

U.S. Treasury General Account (The U.S. government's "bank account" at the Federal Reserve):

June 29 (past newsletter issue): $465 billion

June 13 (current newsletter issue): $543 billion

️↗️ Increase of $78 billion

Over the past two weeks, financial liquidity has increased in the U.S. financial system. Globally, money supply has also increased slightly, from $99.29 trillion to $100.82 trillion. In June, it was China which lowered the benchmark interest rate. As a result, they have improved credit conditions and, consequently, Chinese banks have lent more. For example, newly approved bank loans totaled 3.05 trillion yuan ($421 billion) at the end of June, up from CNY 1.36 trillion ($190 billion) in May.

As indicated in recent issues of Liquidity Corner, then, the Chinese government wants to continue to fuel its economy with cheap money. All it needs is a weak U.S. dollar, because that is the only way to prevent its own expansionary monetary policy from blowing up in its face.

It is precisely this weakening US dollar that the Chinese have now received. The US key currency, or more precisely the DXY index, has just fallen below the magic mark of 100 again. Thus, it is likely before the main reason for this may be the disinflationary trend, which is leading to expectations of a cooling of the economy, so that capital is currently again flowing so strongly out of the U.S. dollar into other assets:

At present, it seems to be the weakening U.S. dollar in particular that is keeping risk assets in line. Financial liquidity also continues to make its contribution - first and foremost BTFP emergency loans. As a look at the rising interest rate on BTFP loans (indicating higher demand) compared to the U.S. equity market shows: The two seem to be marching pretty much in lockstep at the moment.

🟢 Ripple: The outsider that everyone is now cheering for

written by Pascal Hügli

Every crypto connoisseur knows about the tribalistic pack formations: There are Bitcoiners, Etherians, Solana fanboys, IOTA disciples, and more. All of them give each other shit on Twitter again and again - except against one enemy from their own ranks they unite their forces and don't leave a good hair on his head: Ripple and the XRP army.

For many crypto enthusiasts, Ripple is not a crypto project and XRP is not a cryptocurrency. The main criticism has always been the centralization that the project and its infrastructure have been accused of (we have dealt with Ripple in a bit more detail here). In this sense, Ripple and XRP have always been the bogeyman of the service - although, viewed neutrally, it is partly not clear why this project in particular is being scolded so strongly and others projects (which are just as centralized) are not.

Be that as it may, Ripple is currently receiving more support from the crypto world than ever before. This is because it looks like the company might have just won a significant victory in its battle against the US Securities and Exchange Commission (SEC).

Let’s remember: In December 2020, Ripple was accused by the SEC of conducting an unregistered securities offering in the amount of over one billion US dollars. Upon the announcement of this accusation, XRP's price plummeted dramatically, in part because major crypto exchanges like Coinbase removed the coin from their platform. For almost three years, Ripple and its lawyers were now in a legal battle to prove to the world that XRP was not actually a security.

On Thursday evening Swiss time now suddenly came the announcement, according to which a court in the USA had found that XRP is not a security. The price of the coin exploded thereupon and rose in a few hours by up to 80%. Other cryptos such as SOL, MATIC, ADA and XLM also saw sharp price increases. It was mainly those altcoins that reacted to this news that had been classified as securities in the SEC's charges against Binance and Coinbase just a few weeks ago.

Here is a brief summary of the nuances of this decision:

In what is known as a summary judgment - when a court finds that the issue can be resolved without an actual court trial - the U.S. Court in the Southern District of New York considered and ruled on the following four areas:

Institutional sales

Programmatic sales (sales through an exchange)

Other distributions (employee compensation and developer grants)

Insider sales

Only just in the first case, the court ruled that the Securities Act had been violated and Ripple conducted a securities sale by selling XRP to institutional investors. Ripple sold about $728.9 million in XRP in institutional sales and for that it will have to be held liable.

Crucially, and this is the reason why much of the crypto world is so excited, programmatic sales do not constitute securities sales according to the court’s decision. These programmatic sales are about sales that have taken place through a crypto exchange. It is mainly private customers and other public buyers that buy through an exchange and these have bought on the basis of a contract with Ripple XRP, but just through the "anonymized" channel of the crypto exchange itself. These were so-called "blind bid/ask transactions," meaning buyers of XRP could not know exactly where their money ended up (whether to with Ripple, a market maker or an entirely different counterparty), the court said. Using the same reasoning, the court also classified 3 & 4 as non-securities sales.

This is ultimately the most weighty reason put forward by the court. For many crypto investors, it is clear: With this argumentation, other tokens and their projects that distribute their token via a crypto exchange should also be strengthened in their assumption not to justify a securities sale with it. Not entirely without irony it can now be readily read on Twitter: Iff XRP is not a security, then other coins (first and foremost Ether) cannot be securities at all:

While the Chief Legal Officer of Ripple is quite sure about his case and he sees it as confirmed that XRP is not a security, other legal experts express their doubts. For example, some believe that this court decision was about the securities sales and not about the token. Their argument is that even if the court found that specific sales made were not securities sales, the token in general could still be classified as a security.

So, how is this situation to be assessed? Victory, partial victory or defeat in disguise?

What is undisputed is that crypto projects that are now being sued by the SEC on these facts will always be able to bring up this court decision, which will give weight to their arguments. Moreover, other courts now have the ability to rule in favor of indicted crypto projects based on another court's dictum. Thus, the chances of success have clearly shifted in the direction of crypto.

Nevertheless, it should be noted: The court's reasoning could be construed as weak by other courts. In particular, the assumption that private investors who bought the coin via a crypto exchange did not buy with the intention of a token price increase dependent on Ripple's efforts could be discarded. This is because ultimately, the current court decision is not yet law (precedent). It therefore does not have to be followed....

🟢 DalliPay - Global payments for SMEs in real time

written by Reto Steimen

Payments for SMEs can quickly become complicated. Unlike private individuals (individual companies), SMEs cannot simply make a transfer in e-banking, but must maintain an accounting system that meets the legal requirements. In the accounts receivable area, invoices issued by the company itself are managed, for which incoming payments are expected. In the accounts payable section, invoices received are organized, for which payments must be made from the company's own bank accounts. The data exchange with the banks used regarding payments to be sent and received must be actively managed in each case.

For SMEs today, there are various hurdles in the payment system, such as:

Payments at night, weekends and holidays are usually not or only limited available in the banking system. More urgent express processing may incur additional fees. Instructed execution times can be changed unilaterally by banking systems (e.g. for weekends), which can cause discrepancies between the banking system and the bank's own accounting.

For international payments, conversion rates are unknown in advance. Processes in the accounting system must be paused until this information has been communicated by the bank. This can take some time. Depending on the recipient, significant fees may be incurred for international payments.

Direct bank integration (Open Banking), if offered at all, often involves too much extra work and additional costs for SMEs. By manually uploading and downloading payment files from e-banking, internal processes can be poorly optimized. During the execution time on the part of the bank, one’s own processes are interrupted. If several banks are involved, the situation is further complicated.

DalliPay replaces the bank in the payment system of SMEs

As a payer, ISO20022 pain.001 XML files can be exported from the financial program and read into DalliPay. A video explanation can be found here. Payment instructions are converted into crypto payments and transferred to the recipient's assigned wallet. Nationally and globally. In real time. At night, on weekends, and on holidays. With transaction fees well below 0.01 EUR. Any conversion rates are displayed during execution, eliminating the need to pause accounting processes. There are no additional or hidden fees for this.

As a receiver, received crypto payments can be converted into ISO20022 camt.054 XML files and exported. These incoming payments from debtors are then imported into the financial program as usual. Both the export of pain.001 files from and the import of camt.054 files into the existing financial program work the same for users as when payment information is exchanged with a bank.

Why does DalliPay not yet support Bitcoin (L1) or Bitcoin Lightning (L2)?

Unlike XRPL or Ethereum, Bitcoin does not use an account-based model, but a UTXO model. As a result, the sender of a transaction cannot be clearly determined from the recipient's perspective. Even with Lightning as an L2 system, the sender is not clear.

Incoming payments that cannot be clearly assigned to a receivable or a business partner in the accounting system become a problem. Since the sender is unknown, it is neither possible to contact the payer nor to transfer back the received amount. Various solutions are conceivable. However, further additional systems would have to be created for a target-oriented implementation. Adaptations in other software programs used by an SME could also become necessary for easy use.

About the author:

Reto Steimen is the founder of radynamics. With DalliPay, he wants to make SME payments better. For example, the software enables interoperability between ISO 20022 file formats and cryptocurrency payments. It aims to facilitate the sending and processing of received crypto payments within the ISO 20022 capabilities of existing financial software.

🟢 Meme section